The Mortgage Process

Demystifying Mortgages

If you haven’t experienced it before, the mortgage process can feel overwhelming, but our agents will help you stay informed throughout the process, from pre-approval to closing. The first thing to do is consult with a mortgage specialist (or two). If you don’t already have someone in mind, we partner with some of the best lenders in the industry, and we’d be happy to introduce you, so you’ll be taken care of.

Know Your Mortgage Payment

Based on the home's sale price, the term of the loan, buyer's down payment percentage, and the loan's interest rate, this calculator can help estimate what you'll need to pay out monthly for your new home. This calculator factors in PMI (Private Mortgage Insurance) for loans with less than a 20% down payment, as well as town property taxes and its effect on the total monthly mortgage payment.

Buying a home is a big step! Whether you're buying your first home, your dream home, or your tenth investment property, yours will be a big investment. We know how important this is to you and we have an army of experts to make sure we find the perfect property for your unique circumstances. Finding the perfect property is just one way we can help you with your real estate purchase.

In order to determine the amount of home you can afford a lender will use your debt-to-income ratio to determine the percentage of your pre-tax income you spend on debt. Your debt ratio will include: monthly housing costs, car payments, credit cards, student loans, and any other installment debt. If you take on more debt before buying a home it will have an impact on the amount of the loan that the lender will finance.

Our Preferred Lender

Erik Norcott

Erik is a professional and prides himself in helping people achieve their goals. He has funded hundreds of mortgages and understands that every one of them is unique to the people they are paired with. You can expect sound advice and clarity as you work with Erik. Call or email any time for a free consultation.

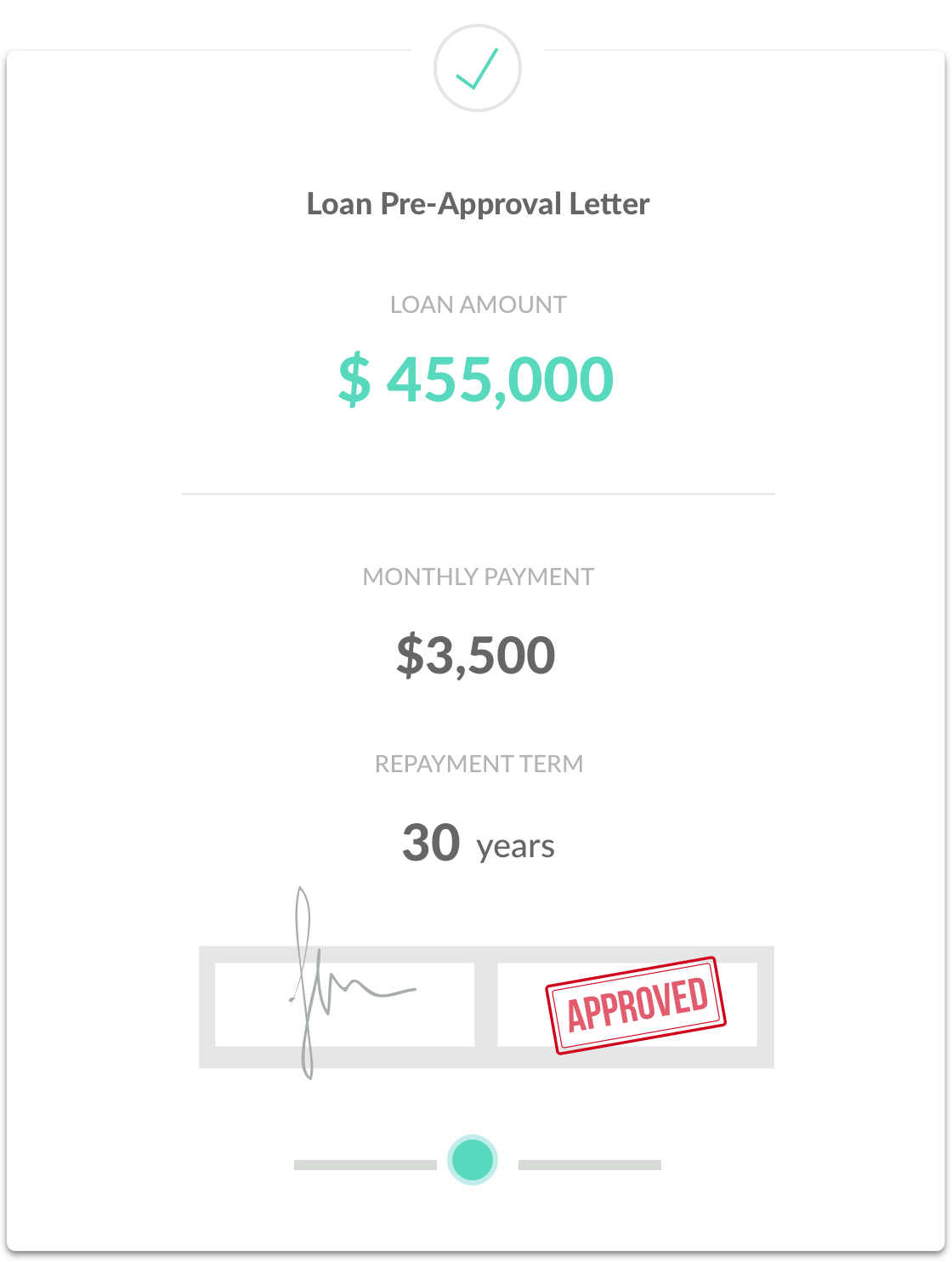

Get Pre-Approval

Before you start looking for a home to buy, it’s a good idea to meet with your Mortgage Officer to get pre-approved for a loan amount. At this stage, the lender gathers information about income, assets and debts of the borrower (you) to determine how much house you may be able to afford. This includes a credit report, pay stubs, Tax documents and recent bank statements. There are a variety of different mortgage programs, so make sure to get pre-qualification for the specific programs that best suit your needs.

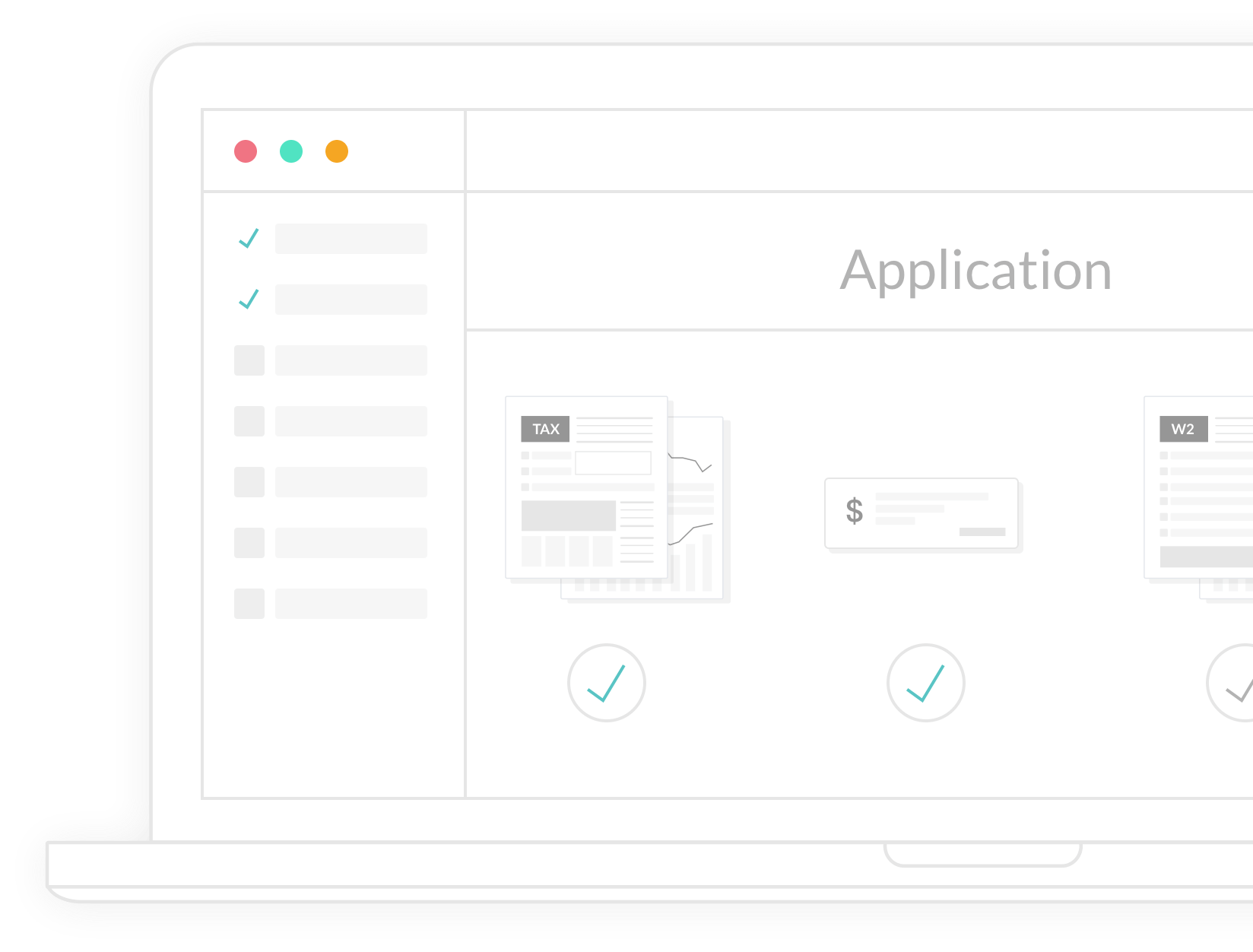

Application & Processing

What happens when a mortgage goes "live"

When you find property you’re ready to buy, your lender will help you complete a full mortgage loan application, and talk you through the various fees and down payment options. The application is submitted to processing, where the documents are reviewed and appraisals and title examination are ordered. Then the mortgage is sent to an underwriter, who reviews and approves the entire mortgage if it meets compliance.

Closing

Signing and Finalizing the deal

Don’t be surprised if you’re asked for additional documentation or clarification throughout the process. Once your mortgage is approved, don’t forget to set up homeowners insurance. Your documents will be sent to the title company, where you’ll sign for the new home and pay any remaining costs. Then the mortgage is recorded and you get the keys. Congratulations, happy homeowner!